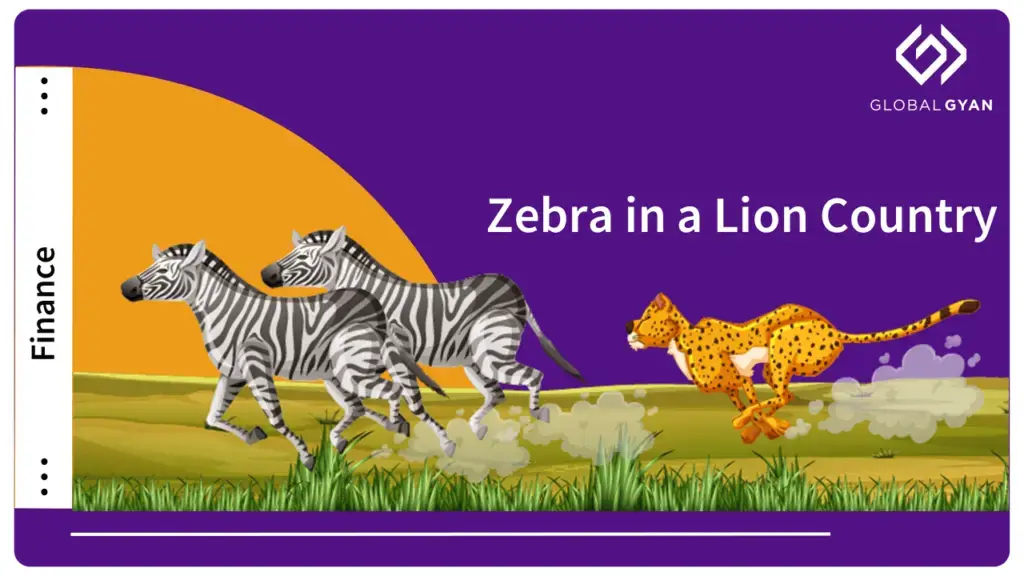

Zebra in a Lion Country

A couple of years ago while browsing through a Crossword store, I came across this book on investing. What caught my fancy at that time was its unique (albeit puzzling) title “ Zebra in a Lion country”. Now what could that possibly mean? I picked up the book to find out more.

Well, turns out that the book was as interesting and unique as its title, if not more.

Just to give some background, the book was authored by Ralph Wanger, who was the lead fund manager of the Columbia Acorn Fund in the US. He managed this fund for an extended 23 years, since its inception in 1970.This fund is credited with being one of the best performing small-capfund in the US during this period, having outperformed the S&P 500.

Here’s what Ralph Wanger has to say in his book

Wanger has very cleverly used the ‘Zebra’ metaphor to equate the behaviour of portfolio managers with those of Zebras. He says that

· Both (the Zebras and the Managers) move in herds and look alike and think alike.

· The key decision for a Zebra is where to stand in a herd. The centre of the herd is the safest for the Zebra, in case a lion attacks, but then the grass is not fresh and green there.

· On the other hand, the outside of the herd has the best grass but the Zebra risks being attacked by a Lion.

· Similarly both (Managers and Zebras) dislike risks but set high goals for themselves.

· The portfolio manager aims for above-average returns while the Zebra wants to eat fresh grass.

· The portfolio manager is at the risk of being fired while the Zebra is at the risk of being eaten by a Lion.

The moral of the story is: whatever be the situation (whether you are a Zebra or a Manager), if you want above-normal gains you have to differentiate yourself from peers i.e take a certain degree of risk and venture into unfamiliar territory.

i.e If you want to stand out from the pack, you have to stand OUTSIDE the pack!

While Wagner used this analogy to highlight his investment philosophy (focused on investing in small and mid-cap stocks) the same hypothesis can be applied to any industry. In fact, nothing can be truer than this when it comes to the banking industry today.

Here is what I mean

Most banks today act like Zebras – They look alike, lend to similar segments and have similar business models with hardly any differentiation in their products and services.

Moreover all banks prefer to stay at the center of the herd (i.e. targeting the safer affluent customer) but no one wants to lend to the riskier SME or the unbanked rural population for fear of credit losses.

Can banks sustain their profitability or even growth if they fail to differentiate? What would happen if they dared to stand outside the pack?

Do we know of any Zebras in the banking industry who dared to stand outside the pack? So were they eaten by the Lion or did they enjoy the green grass?

Well, here is a unique story of Bandhan Bank, a first-of- its-kind example of a micro-finance institution transforming to a universal bank, in India. Bandhan Bank started as a humble micro-finance institution in 2001 to cater to the credit needs of the small and marginal women entrepreneurs in rural West Bengal. The rural population had no access to formal credit and were being misled by moneylenders, the latter often charging exorbitant interest rates (around 8%-10% per month) and without any transparency in dealings. Big organized players like Banks and NBFC’s were wary of lending to these poor people, as that meant lending without any credit history and without collateral.

Bandhan not only bucked the trend by creating a leader in the micro-lending space with its indigenous door-to-door service model, it also emerged as the ultimate winner in the eyes of the regulator when it got the banking license, for this very reason – proven track record of lending to the poor and the un-bankable segment of the society.

What’s interesting to note is that while established banks today are largely tapping customers at the top of the pyramid (micro-finance lending being only a small part of their portfolio), Bandhan Bank’s entire portfolio comprises people from the bottom of the pyramid. Despite playing safe, the so called established banks are saddled with huge amounts of bad debts (gross NPA of ~10%) whereas Bandhan Bank has a gross NPA of ~1% despite lending to the riskier segments of the society. Bandhan Bank challenges the conventional wisdom of what constitutes a credit worthy customer. It also reinforces the fact that even social businesses can be run profitably, if one has deep understanding of the customer’s need.

-Saumya Agarwal is Manager- Research and Content Development at Globalgyan. She has over 11 years experience in financial services primarily as an equity research analyst and a credit research analyst for banks & financials. She has worked with reputed organizations such as JPMorgan, HSBC Securities and CRISIL. She is an avid reader, loves to play badminton and is a travel enthusiast.